Finance Automation for Property & Real Estate in Australia: How Agencies, Developers & Strata Managers Streamline Trust Accounting, AP & Reporting

Ordron26 min read

Property finance sits in a different risk category to almost every other industry in Australia. The moment rental income or buyer deposits land in a trust account, your team is operating under state legislation with real consequences for breaches: licence suspensions, fines, and criminal liability in serious cases. That is before you account for the sheer volume of transactions a busy rent roll generates, the multi-entity complexity of a strata scheme or development portfolio, and the monthly pressure of reconciling disbursements down to the cent.

Most finance automation content online treats property the same as any other vertical. It is not. The compliance obligations are sharper, the reconciliation requirements are more granular, and the downstream consequences of an error are more severe. If your team is still processing rental receipts, owner disbursements, and trust reconciliations largely by hand, the risk is not just the hours lost. It is the exposure that builds every month in a spreadsheet or manual process that was never designed to scale.

This article is a practical guide to finance automation for Australian property businesses: real estate agencies managing rent rolls, strata managers handling levy receipts and fund disbursements, and property developers managing multi-entity AP and project reporting. I will cover what is genuinely automatable today, where human sign-off remains non-negotiable, and how to integrate automation into platforms your team already uses rather than replacing your stack. No aspirational projections. Just what the work looks like and what it returns, measured after go-live.

Key Takeaways

- Trust accounting automation can materially reduce reconciliation time and error rates, but compliance sign-off under state legislation remains a human responsibility.

- Rental receipt processing and owner disbursement workflows are among the highest-volume, highest-value automation targets on a typical rent roll.

- AP automation across managed properties and development projects follows the same logic as general AP automation but requires property-specific coding rules and multi-entity handling.

- Consolidated reporting for strata schemes and multi-entity portfolios is one of the most time-consuming tasks in property finance and one of the most straightforward to automate.

- Integration with platforms like PropertyMe, Console Cloud, Xero, and MYOB is achievable without replacing any existing system.

- Quick wins exist in almost every property finance operation. Identify and ship them first before expanding scope.

Summary Table: Process Pain, Automation Outcome, and Typical Time Saved

| Process | Common Pain Point | Automation Outcome | Typical Time Saved |

|---|---|---|---|

| Trust account reconciliation | Manual daily/monthly matching, audit trail gaps | Automated matching, timestamped audit log | 60-80% of reconciliation time |

| Rental receipt processing | Manual data entry from bank feeds into PM software | Automated receipt capture and GL coding | 70-85% of processing time |

| Owner disbursement runs | Manual calculation, PDF statement generation, approval chasing | Automated calculation, statement generation, approval workflow | 50-70% of disbursement cycle |

| Accounts payable (managed properties) | Manual invoice coding across multiple properties and owners | OCR capture, property/owner coding, exception routing | 65-96% cycle time reduction |

| Levy receipts (strata) | Manual reconciliation of levy payments to lot owner ledgers | Automated payment matching, arrears flagging | 60-75% of manual matching time |

| Multi-entity consolidated reporting | Manual export, reformat, and consolidation across entities | Automated consolidation, on-demand reporting | Overnight lag to same-day or on-demand |

| Bank reconciliation | Manual statement import and matching in Xero/MYOB | Automated rule-based matching with exception queue | 80% reduction in reconciliation hours |

Why Property Finance Is Harder Than Other Verticals

I work across eight industries. Property finance consistently has the most complex compliance obligations sitting directly inside the core financial workflow. In manufacturing or logistics, compliance tends to live at the edge: tax reporting, payroll, WHS. In property, it lives at the centre. Every rental receipt, every disbursement, every trust account balance is a regulated transaction.

Here is what makes the property vertical structurally different from a finance automation perspective.

Trust accounting is legislated, not just best practice

In New South Wales, the Property and Stock Agents Act 2002 and its regulations set out precise requirements for how trust money must be received, held, reconciled, and disbursed. The NSW Fair Trading regulator audits agencies, and breaches can result in licence suspension. Victoria's Estate Agents Act 1980 carries similar obligations, enforced by Consumer Affairs Victoria. Queensland's Property Occupations Act 2014, South Australia's Land Agents Act 1994, and Western Australia's Real Estate and Business Agents Act 1978 each have their own requirements. The details differ by state, but the principle is consistent: trust money is not your money, the reconciliation must be current, and the audit trail must be defensible.

This means any automation you introduce into trust accounting must produce records that satisfy a regulator audit, not just records that satisfy your own reporting. That is a higher bar than most industries face.

Transaction volumes are high and growing

A rent roll of 300 properties generates thousands of individual transactions per month: rental receipts, disbursements, maintenance invoice payments, landlord fee deductions, bond lodgements, and adjustments. At 500 properties, the manual reconciliation burden is significant. At 1,000 or more, it is unsustainable without automation or significant headcount. The ABS reports that approximately 30% of Australian households rent privately, representing a large and structurally durable transaction base for agencies that manage residential portfolios.

Multi-entity and multi-fund complexity

Strata managers operate with separate administrative funds and capital works funds (sinking funds) for each scheme, each with its own levy schedule, its own bank account, and its own reporting obligations under the relevant strata legislation in each state. A strata management firm handling 50 schemes is effectively operating 100 or more separate accounting entities simultaneously. Without automation, the consolidation and reporting burden alone consumes enormous amounts of finance team time.

Developers add another layer: project-level cost tracking, progress claim management, multi-entity intercompany transactions, and the need to produce consolidated group accounts across entities that may sit in Xero, MYOB, or a legacy ERP.

Human error risk is asymmetric

In most industries, a coding error in AP costs you time to fix. In property trust accounting, a misallocation can trigger a compliance issue. The asymmetry between the cost of an error and the cost of preventing it is one of the clearest justifications for automation investment in this vertical.

Trust Accounting Compliance and Audit-Trail Automation

Let me be direct about what automation can and cannot do here. Automation can eliminate the manual steps that currently sit between a trust account transaction and a compliant, reconciled ledger. It can generate timestamped, immutable audit logs that show exactly when each transaction was received, coded, matched, and reconciled. It can flag discrepancies the moment they appear rather than at month-end. What it cannot do is replace the authorised officer's responsibility to sign off on trust account reconciliations under state law. That sign-off remains a human responsibility. A well-designed automation makes that sign-off faster, more confident, and better evidenced. It does not remove it.

For more on building automation with a defensible audit trail, see our detailed guide on finance automation and compliance audit trails in Australia.

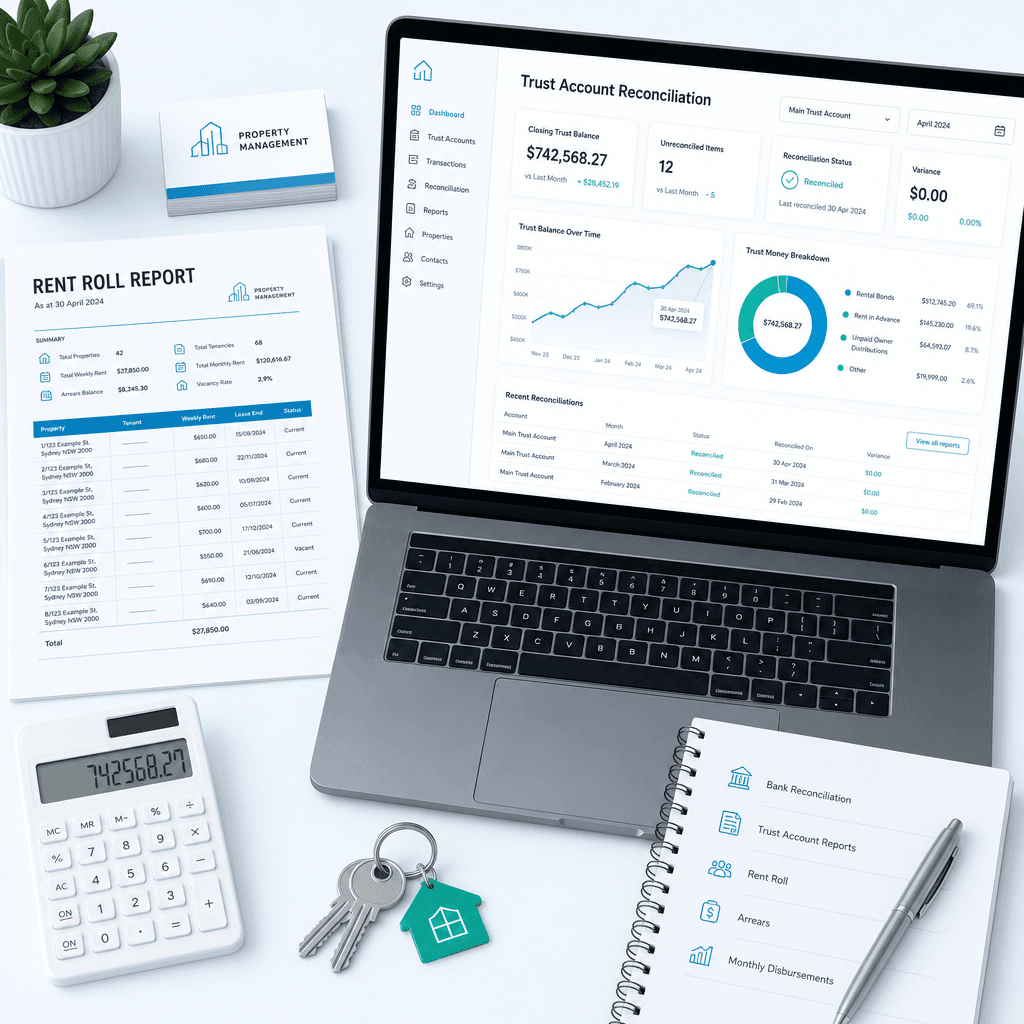

What an automated trust accounting workflow looks like

A practical trust accounting automation layer typically handles the following:

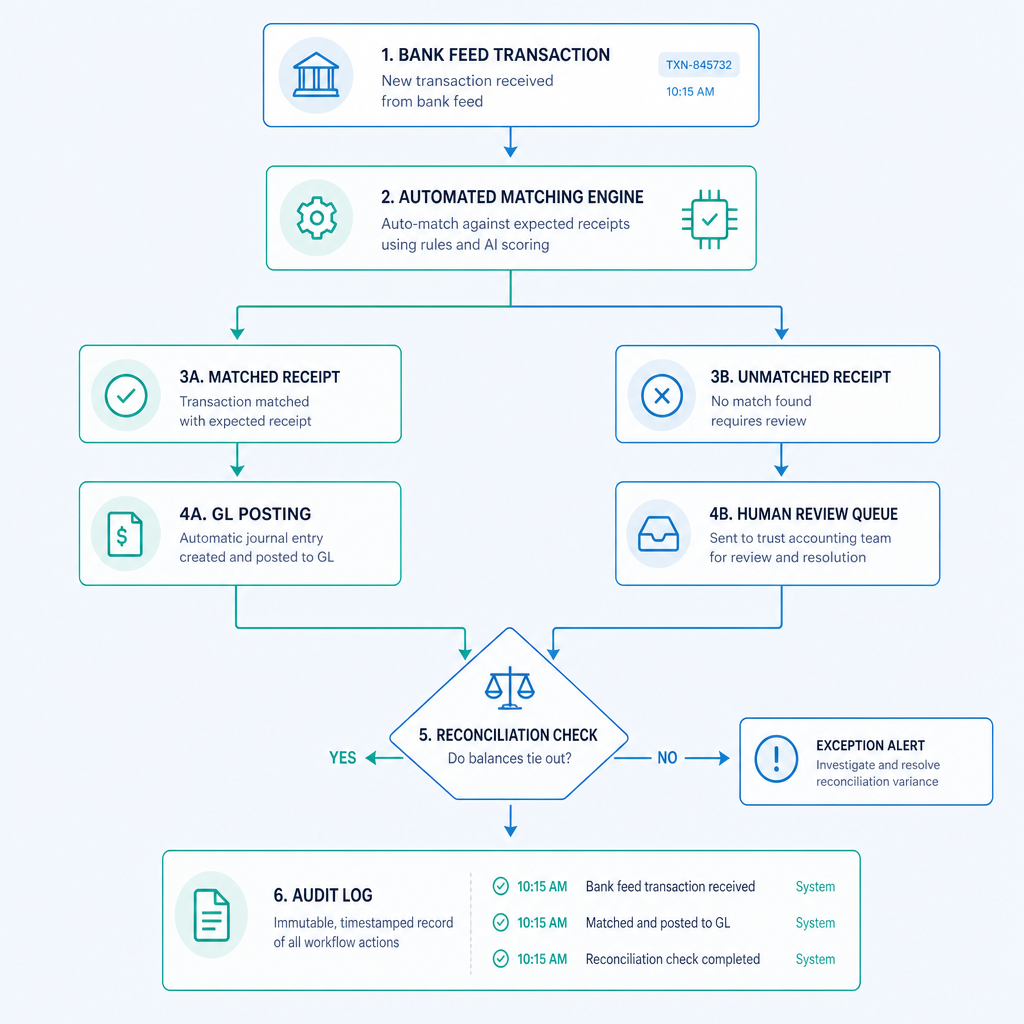

Receipt capture and coding. Bank feed transactions are captured, matched to the correct tenancy and property, and coded to the trust ledger automatically. Where a receipt cannot be matched with sufficient confidence, it is routed to a human reviewer. The system routes only genuine exceptions to humans, not every transaction.

Disbursement calculation. At each disbursement run (weekly, fortnightly, or monthly depending on your practice), the system calculates net owner amounts after deducting management fees, maintenance invoices, council rates, and other deductions, and prepares disbursement batches for review and approval.

Reconciliation. The trust account balance is reconciled against the sum of trust ledger balances automatically, with any variance flagged immediately. The reconciliation timestamp, the balance figures, and any exceptions are logged in a format that supports a regulator audit.

Audit trail. Every action taken by the system is logged: who approved what, at what time, with what data. This is not a nice-to-have in property trust accounting. It is a compliance requirement.

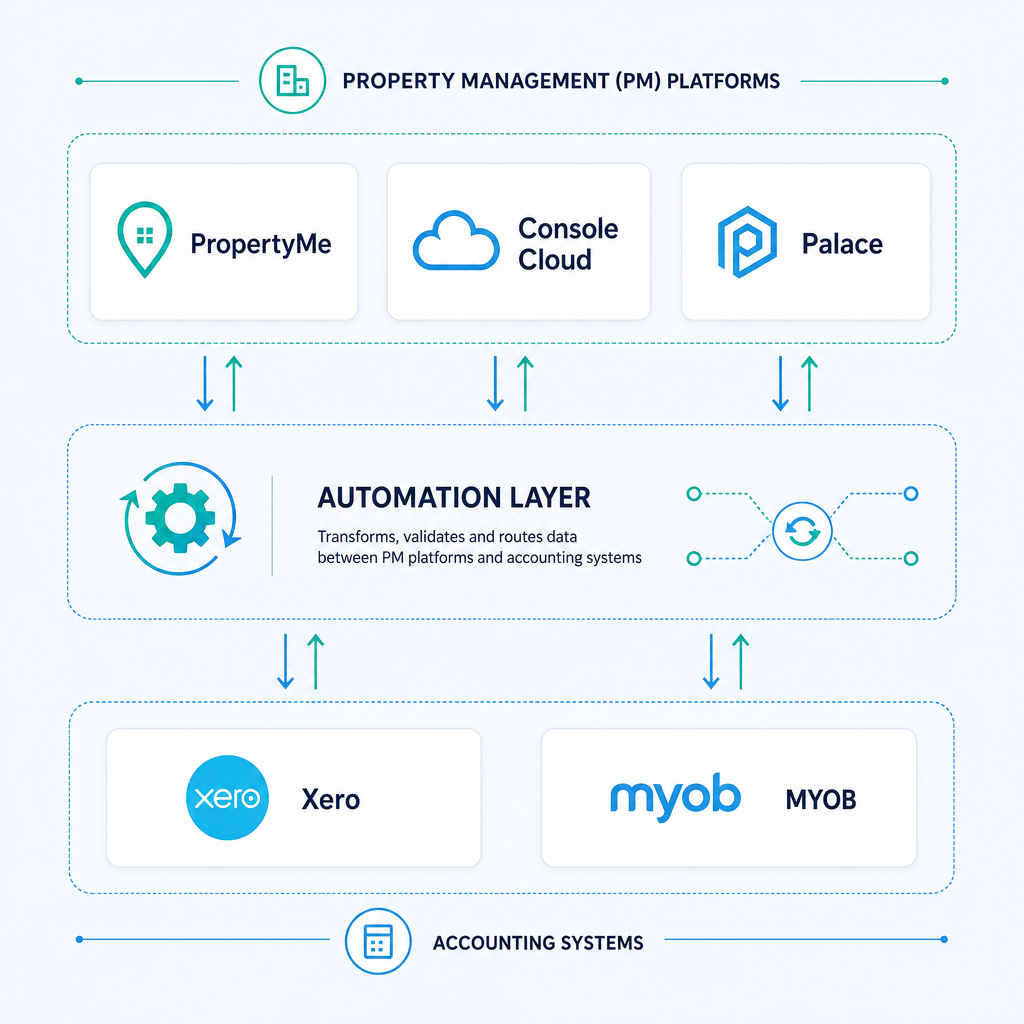

For agencies using PropertyMe, Console Cloud, or Palace, the trust accounting ledger is already managed within the platform. The automation layer sits above it, handling bank feed matching, disbursement batch preparation, and reconciliation reporting without touching the core ledger logic that the PM platform manages. I will come back to integration specifics in a later section.

A practical caveat. State regulators including NSW Fair Trading and Consumer Affairs Victoria have not published specific guidance on automated trust accounting processes at the time of writing. Agencies should seek advice from their state's real estate institute or a compliance specialist before implementing any automated process that touches trust money. The Real Estate Institute of Australia (REIA) and state REI bodies are the appropriate reference points for current compliance requirements.

Automating Rental Receipts and Owner Disbursements

Rental receipt processing and owner disbursements are the highest-volume workflows in a residential property management business. They are also among the most automatable, because the rules governing them are consistent and deterministic: rent is due on a specific date, at a specific amount, from a specific tenant, for a specific property. That structure is exactly what rules-based automation handles well.

Rental receipt processing

The manual workflow typically looks like this: bank statement arrives, staff match each receipt to the correct tenancy in the PM software, code it correctly, update the ledger, and flag any short payments or unidentified deposits. On a rent roll of 300 properties with a weekly or fortnightly payment cycle, this can consume multiple hours of staff time per week.

An automated receipt workflow connects the bank feed directly to the PM platform and the accounting system. Receipts are matched to tenancies by reference number, amount, and bank account. Matching logic handles common variations: rounded amounts, partial payments, split payments from joint tenants. Unmatched receipts, short payments, and new references are routed to a human reviewer with the context they need to resolve the exception quickly. Matched receipts are coded and posted without manual intervention.

The practical outcome for agencies that have gone through this process is a reduction in manual processing time of 70-85% on receipt workflows. A property manager who was spending two to three hours per week on receipt matching is now spending fifteen to twenty minutes reviewing exceptions. That time goes back into landlord and tenant relationships, which is the part of the job that drives retention.

Owner disbursements

Disbursement runs are more complex than receipt processing because they involve calculation, not just matching. The system needs to know the gross rent received, the management fee rate, any maintenance invoices approved for payment, any deductions for council rates, water, insurance, or other landlord expenses, and the net disbursement amount. It then needs to generate a statement for the landlord, prepare the payment instruction, and log the disbursement against the trust ledger.

Automation handles each of these steps. Management fee schedules are stored in the system and applied automatically. Approved maintenance invoices are deducted. Statements are generated and delivered by email. Payment instructions are prepared for review and approval before processing. The human step is reviewing and approving the disbursement batch, not building it.

For a mid-sized agency with 400 properties running fortnightly disbursements, the time saving on disbursement preparation alone can exceed ten hours per fortnight. Over a year, that is more than 250 hours returned to the business.

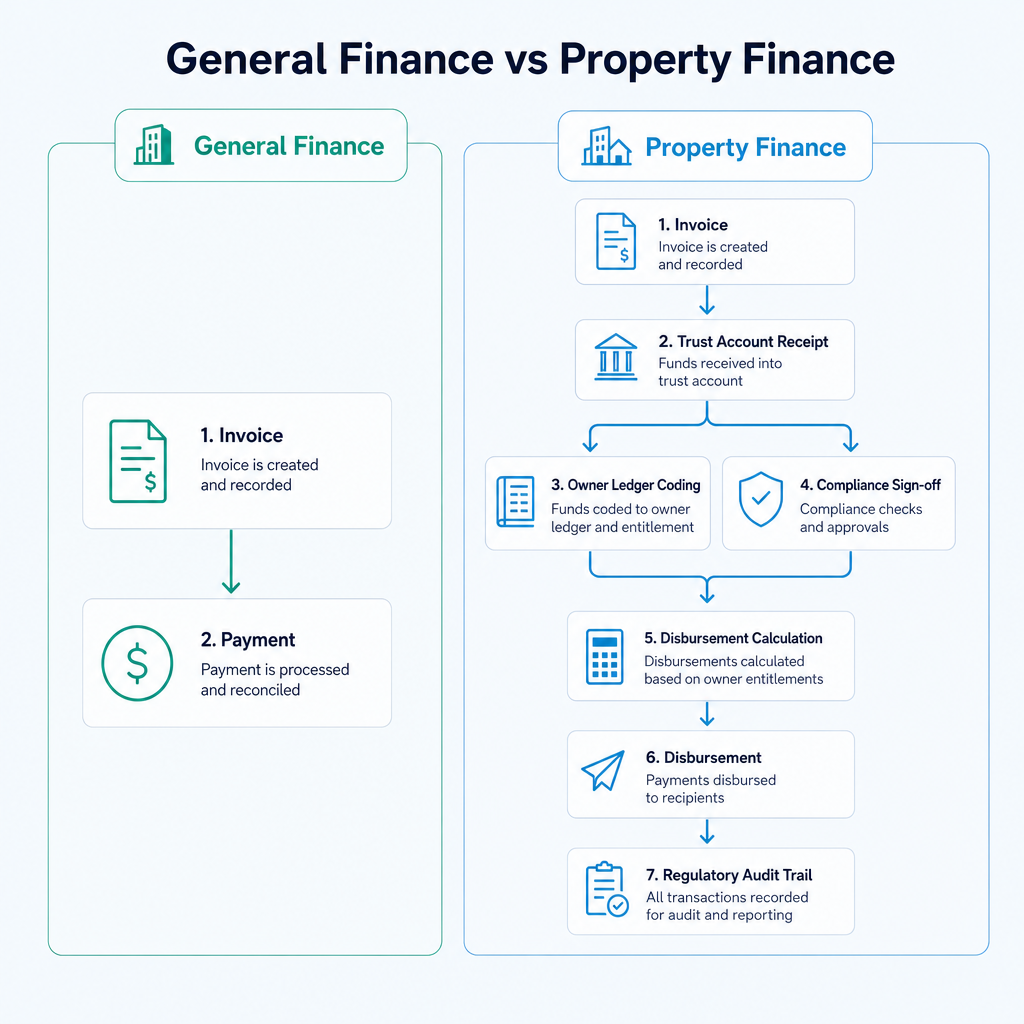

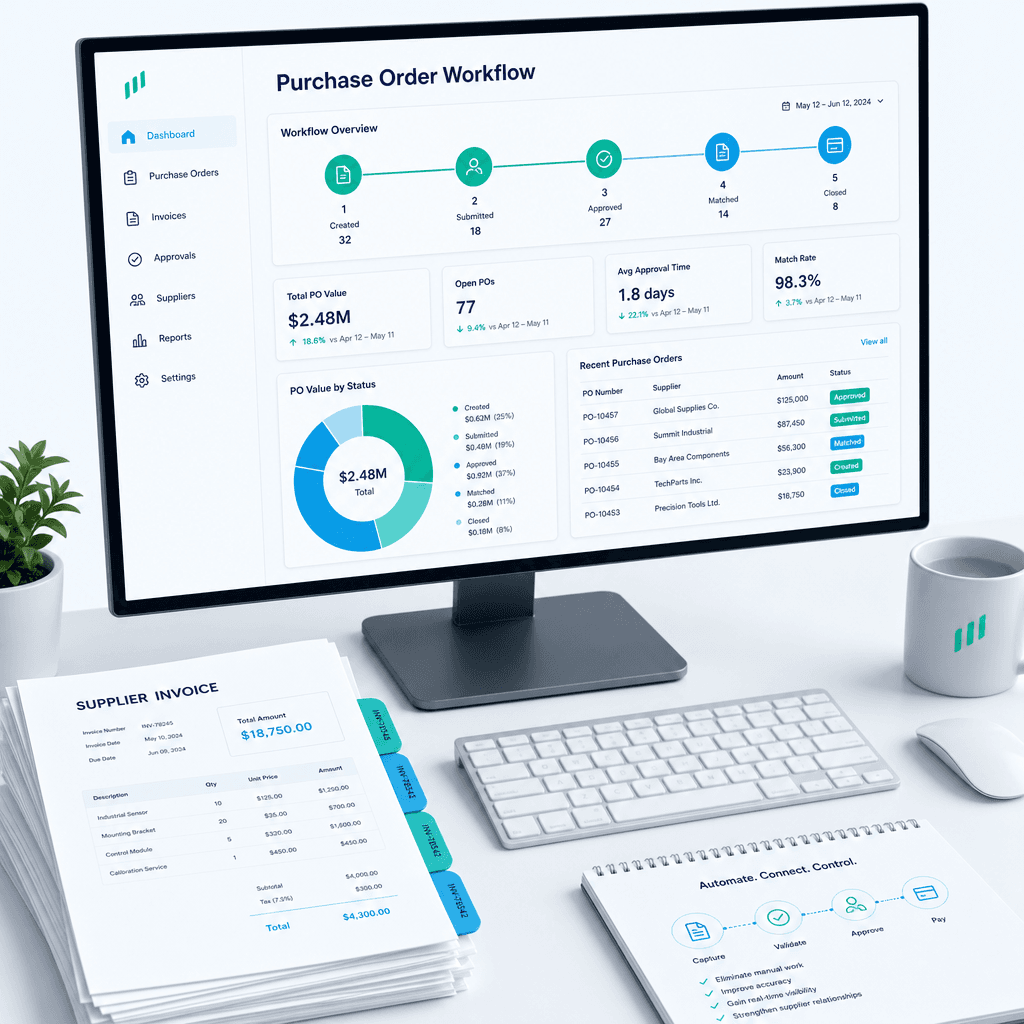

AP Automation Across Managed Properties and Developments

Accounts payable for property businesses has a specific complexity that general AP automation guides do not address: every invoice needs to be coded not just to a GL account but to a specific property, a specific owner, and often a specific fund or cost centre. A plumbing invoice for 14 Smith Street needs to land against the correct landlord's disbursement ledger, not just against a generic maintenance expense account.

This coding requirement means property AP automation needs property-aware logic, not just generic OCR and GL coding.

How property AP automation works in practice

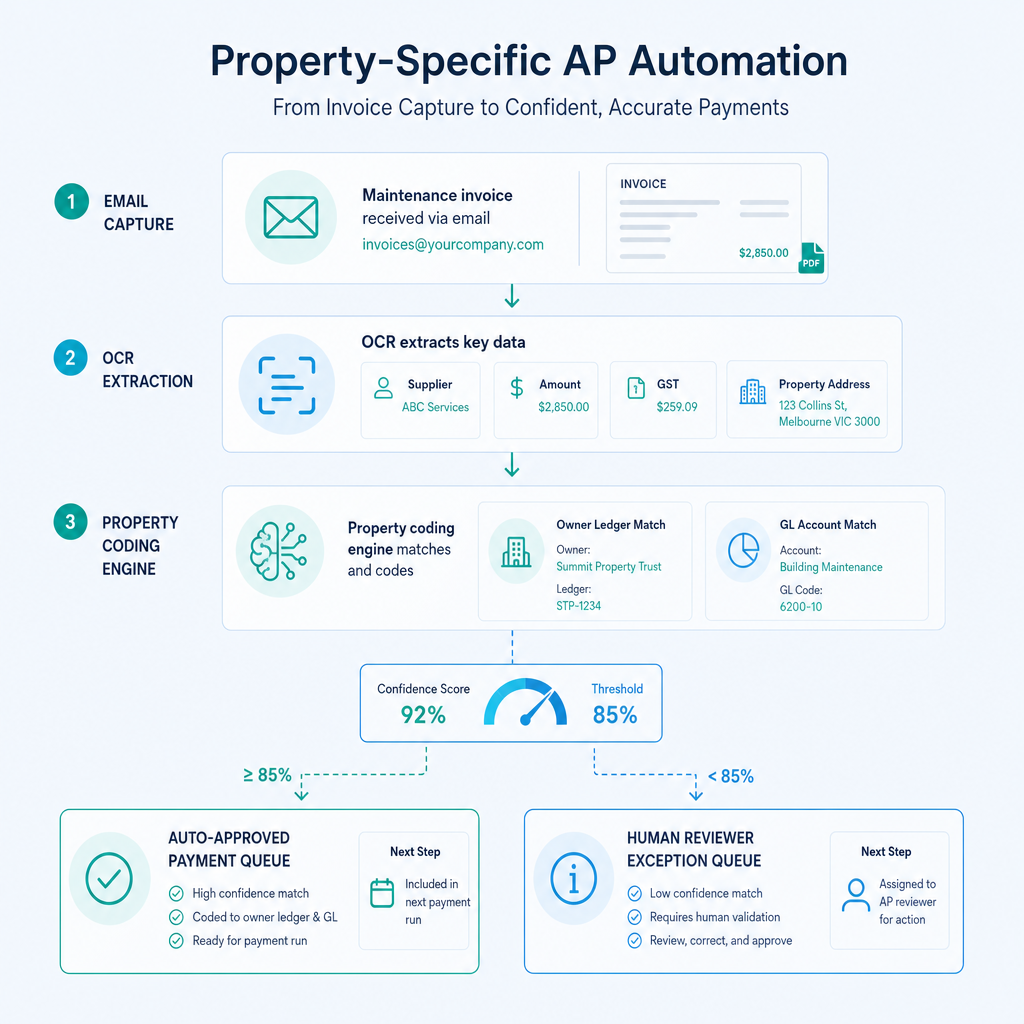

The process starts with invoice capture. Maintenance invoices, council rates notices, water usage bills, insurance renewals, and body corporate levies arrive by email, post, or supplier portal. An OCR layer reads the document, extracts the key fields (supplier, amount, GST, due date, property address or reference), and passes them to a coding engine.

The coding engine matches the property reference to the correct owner and fund in the PM platform, applies the correct GL treatment, and prepares the invoice for approval. Where the match is confident and the amount is within pre-approved limits, the invoice routes directly to the payment queue. Where there is ambiguity, such as an invoice with a partial address or an amount above threshold, it routes to a human reviewer.

In our enterprise AP engagements across other verticals, we have achieved coding accuracy above 95% and cycle time reductions of 65% or more. I have documented a case where a national operator's AP batch time dropped from four hours to fifteen minutes per batch after plugging OCR and workflow logic directly into their existing process without introducing any new software platform. The property vertical has the same opportunity, with the addition of property-level coding as a specific automation target.

For more detail on how invoice automation works technically, see our guide on invoice automation in Australia.

Development AP

For property developers, AP automation needs to handle progress claims, retention calculations, variations, and cost-to-complete tracking across multiple projects and entities. Progress claims from builders or contractors are typically high-value, require certification before payment, and need to be coded to the correct project and cost category.

Automation does not replace the certification process (that requires a human with the appropriate authority), but it handles everything around it: capturing the claim document, extracting the key fields, matching it to the contract and the project budget, flagging any variance, preparing the payment instruction once certification is received, and posting the transaction to the correct project ledger. The human focuses on the certification decision, not the administrative processing.

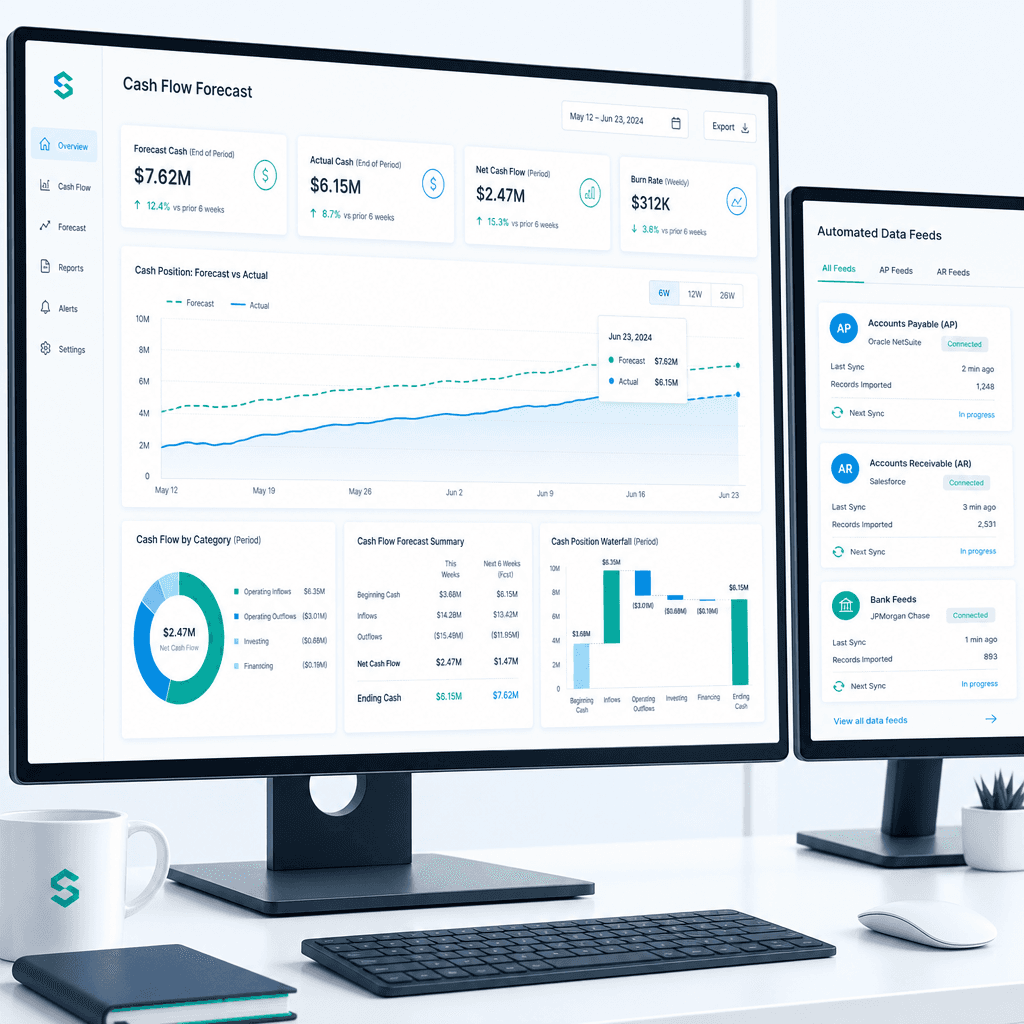

Multi-Entity and Strata Reporting Consolidation

Consolidated reporting is one of the most time-consuming tasks in property finance and, in my view, one of the most underrated automation targets. Most property finance teams have been living with the pain for so long that they have normalised it.

For a strata management firm with 60 schemes, producing a monthly report for each scheme means pulling data from 60 separate ledgers, formatting it consistently, checking it for anomalies, and distributing it to the relevant owners corporation committee. Multiply that by 12 months and add in levy budget comparisons, arrears reports, and capital works fund balance tracking, and you have a substantial ongoing reporting burden.

For a residential agency, the equivalent is the monthly owner statement pack: generating, checking, and distributing hundreds of individual statements across the rent roll, alongside portfolio-level reporting for the principal and any investor clients with multiple properties.

Automation addresses both. Reporting templates are configured once. Data is pulled directly from the source systems (PM platform, accounting system, bank feeds) on a scheduled or on-demand basis. Reports are generated, checked against pre-set validation rules (for example, fund balances must be positive, levy arrears above a threshold trigger a flag), and distributed automatically.

The outcome is not just time saved. It is the shift from overnight or end-of-week reporting to on-demand reporting. One distribution group I worked with had been waiting until the next morning for management pack data. After automating the reporting layer across their Xero environment and operational systems, the same reports were available before 8 a.m. without anyone building them overnight. The same principle applies in property: a strata manager can pull a current fund balance report at 10 a.m. on a Tuesday before a committee call rather than waiting for a staff member to compile it.

For more on automating financial reporting in Australian businesses, see our guide on financial reporting automation in Australia.

Integration With Xero, MYOB, and Property Management Platforms

One of the most common questions I receive from property finance teams is whether automation requires replacing their existing PM platform or accounting system. The answer is no, and I would argue that replacing working systems is almost never the right starting point.

PropertyMe, Console Cloud, and Palace all have API capability or data export structures that allow automation to read from and write to the platform without replacing it. Xero and MYOB both have well-documented APIs. The automation layer sits between these systems, orchestrating data flows rather than becoming the system of record.

Here is what a typical integration architecture looks like for a residential agency:

- PropertyMe or Console Cloud remains the system of record for tenancy data, trust ledgers, and owner disbursements.

- Xero or MYOB remains the accounting system of record for the agency's own P&L, GST, payroll, and reporting.

- The automation layer handles bank feed matching, disbursement batch preparation, AP invoice processing, and reporting consolidation, passing data between the PM platform and the accounting system without manual re-entry.

The integration does not require either system to be replaced or upgraded. Where a PM platform lacks a direct API for a specific data point, RPA (robotic process automation) can drive the platform interface directly, reading and writing data the same way a staff member would but faster, at higher volume, and without errors from fatigue.

I have worked with businesses running twenty-year-old systems with no APIs and returned over 160 hours per month to their finance teams without introducing a single new software licence. The principle holds in property: you do not need a new platform to automate your workflows. You need a well-designed integration layer that bridges what you have.

For a detailed look at bank reconciliation automation within Xero and MYOB, see our guide on how to automate bank reconciliation in Xero and MYOB in Australia.

A note on data integration outcomes

Our asset management data integration case study details how we handled multi-source data integration for a complex asset management operation, including the specific approach to validating data across systems before it is written to the accounting ledger. The property vertical faces the same data quality challenges: PM platform data, bank feed data, and accounting system data need to agree before any automated posting is made. The validation logic is not glamorous, but it is the difference between automation that works and automation that creates a new category of error to clean up.

Realistic Implementation Considerations and Limitations

I want to be direct about what implementation looks like in practice, because the gap between a demo and a running system is where most property automation projects either succeed or stall.

Start with a focused scope

The temptation in property finance automation is to try to automate everything at once: trust accounting, AP, reporting, disbursements, levy receipts, all in one project. That approach tends to produce large, slow projects that deliver nothing measurable for six to twelve months and then struggle to get over the line because scope has grown faster than momentum.

The approach that works is to identify the two or three highest-value automation targets in your specific operation, ship those first, measure the outcome, and then use that credibility to expand scope. For most property management businesses, the highest-value targets are rental receipt processing and disbursement batch preparation, because they are high-volume, highly repetitive, and directly connected to the workflows that consume the most staff time. Quick wins are real. Find yours and build from there.

Compliance sign-off is non-negotiable

I noted this earlier but it bears repeating in the implementation context. Every state's trust accounting legislation requires an authorised person to sign off on trust account reconciliations. Automation can prepare the reconciliation, flag exceptions, and generate the supporting documentation. It cannot sign off on your behalf. Build your automated workflow so that the human sign-off step is fast and well-evidenced, not so that you have tried to automate around it.

Agencies should also check their professional indemnity insurance requirements and any conditions attached to their licence regarding the use of automated processing in trust accounting. State REI bodies and licencing regulators are the appropriate first point of contact.

Data quality before automation

Automation amplifies what is already in your data. If your PM platform has duplicate tenancy records, inconsistent property references, or historical coding errors, an automated process will encounter these immediately and either fail, route excessive exceptions to human reviewers, or, in a poorly designed system, post transactions incorrectly. A data quality review of your PM platform and accounting system before implementation is not optional. It is the work that makes everything downstream reliable.

Phased rollout and parallel running

For trust accounting automation specifically, I strongly recommend a parallel running period: running the automated process alongside your existing manual process for at least one full reconciliation cycle before relying on the automated output. This gives your team confidence in the system, identifies any edge cases in your specific data, and ensures the audit trail is correct before you depend on it for a compliance purpose.

Realistic timeframes

A well-scoped rental receipt and disbursement automation for a mid-sized agency (200-500 properties) can typically be designed, built, and deployed in six to ten weeks, assuming data quality is acceptable and the integration with your PM platform and accounting system is straightforward. More complex implementations involving strata multi-entity consolidation, development AP, or legacy system integration will take longer. Any vendor or consultant who quotes you two weeks for a full trust accounting automation without having reviewed your data and systems first is not giving you a realistic number.

Cost and return

The cost of property finance automation varies significantly based on scope, the complexity of your systems, and whether you need custom integration work. The return, in our experience across multiple engagements, tends to be measured in hours per month returned to finance and property management staff, error rate reduction, and the indirect value of improved compliance confidence. Those returns are real and measurable. We do not quote projected savings before we have seen your actual workflow. The numbers should be attached to your operation, not to a generic benchmark.

If you want a realistic view of what automation could return in your specific property business, the right starting point is a conversation about your current process, not a product demo. Reach out to the Ordron team to start that conversation.

References

-

NSW Property and Stock Agents Act 2002 and Regulations (NSW Fair Trading). The primary legislative framework governing trust accounting, licence obligations, and conduct requirements for real estate agents and property managers in New South Wales. Available through the NSW Fair Trading website and the NSW legislation portal.

-

Estate Agents Act 1980 (Consumer Affairs Victoria). Victoria's primary legislation for real estate agent conduct, including trust account keeping obligations, audit requirements, and licence conditions. Administered by Consumer Affairs Victoria.

-

Real Estate Institute of Australia (REIA) Trust accounting guidance and compliance resources. The REIA and its state member bodies (REINSW, REIV, REIQ, REIWA, REISA, and REINT) publish guidance on trust accounting obligations, compliance best practice, and professional standards for agents across all Australian states and territories.

-

Australian Bureau of Statistics (ABS): Housing Occupancy and Costs (Catalogue 4130.0). ABS data on residential tenure rates, including the proportion of Australian households renting privately, supporting context on the scale of the residential property management sector.

-

Property Occupations Act 2014 (Queensland Office of Fair Trading). Queensland's legislative framework for property agent licensing and trust accounting obligations, administered by the Queensland Office of Fair Trading.

-

Ordron case study: Asset Management Data Integration (Ordron, 2026). Documents the approach and outcomes of a complex multi-source data integration engagement for an asset management operation, including validation logic, system integration architecture, and measured outcomes. Available at ordron.com/case-studies/asset-mgmt-data-integration.

Frequently asked questions

- Is trust accounting automation legal in Australia?

- There is no prohibition on using automated tools to assist with trust accounting processes in Australia. State legislation sets out the trust accounting obligations, not the specific methods by which they must be met. Automation can assist with receipt processing, ledger posting, reconciliation preparation, and audit trail generation. However, the legal obligation to maintain accurate trust records and have reconciliations signed off by an authorised person remains with the licence holder. Agencies should consult their state REI body and a compliance specialist before implementing automated processes that touch trust money.

- Does finance automation work with PropertyMe and Console Cloud?

- Yes. Both PropertyMe and Console Cloud have API capability and structured data exports that allow an automation layer to read tenancy data, trust ledger balances, and disbursement information, and to push processed data back into the platform. Where specific data points are not available via API, RPA can interact with the platform interface directly. The automation layer does not replace PropertyMe or Console Cloud. It sits alongside them, handling the processing steps that currently require manual intervention.

- Does property finance automation work with Xero and MYOB?

- Yes. Both Xero and MYOB have well-documented APIs that support automated posting, bank feed matching, and reporting extraction. Automation can handle GL coding, bank reconciliation, and management reporting within your existing Xero or MYOB environment without requiring a platform change or upgrade.

- Can automation handle strata levy receipts and arrears management?

- Yes. Strata levy receipt processing follows the same matching logic as rental receipt processing: a payment arrives, it needs to be matched to the correct lot owner and levy period, and posted to the correct fund. Automation handles the matching and posting, flags partial payments or unidentified receipts for review, and can generate arrears reports and levy notices automatically. The arrears follow-up process can also be partially automated through triggered workflow actions based on arrears thresholds.

- What about GST and BAS lodgement for property businesses?

- GST treatment in property finance is complex. Residential rent is GST-exempt. Commercial rent is generally taxable. Automated coding systems can apply GST rules consistently across transaction types, but the rules need to be correctly configured and reviewed by a registered tax agent or BAS agent. Automation reduces the manual coding burden and the risk of inconsistent GST treatment across high volumes of transactions. It does not replace professional tax advice on the correct GST treatment of specific transaction types.

- How long does implementation take for a typical property management agency?

- For a focused scope covering rental receipt processing and disbursement batch preparation for a mid-sized agency of 200-500 properties, a realistic implementation timeline is six to ten weeks from scoping to go-live, assuming data quality is acceptable. More complex implementations involving strata multi-entity consolidation, development AP automation, or legacy system integration will take longer. A parallel running period of at least one full reconciliation cycle is recommended before relying solely on automated outputs.

- Do we need to replace our existing PM platform or accounting system to automate?

- No. The approach is to bridge, extend, and automate what already exists rather than replace it. Your PM platform and accounting system remain in place as systems of record. The automation layer handles the processing steps between them. Replacing working systems carries platform migration risk on top of process change risk, and is almost never the right first step.

- Can a small agency with a rent roll under 100 properties justify automation?

- It depends on the specific workflow and the current pain. For very small rent rolls, some automation targets may not generate enough volume savings to justify a custom build. The better starting point is ensuring the existing PM platform's built-in automation features are fully configured. Custom automation typically becomes clearly cost-effective for rent rolls above 150-200 properties, or for any agency where specific manual processes are consuming disproportionate staff time regardless of portfolio size.

Ordron

Finance automation team, Sydney

Ordron builds the finance automation infrastructure that runs AP, AR, reconciliations and reporting on autopilot for Australian mid-market businesses.

More from the Ordron Insights catalogue

Selected by topic. Updated as the agent publishes.

Cash Flow Forecasting Automation: A Practical Guide for Australian Finance Teams (2026)

If your finance team rebuilds the cash flow forecast from scratch every week or every month, you already know where the time goes. Someone pulls an AR ageing…

Purchase Order Automation: A Practical Guide for Australian Finance Teams (2026)

If your finance team is still raising purchase orders in a shared inbox, chasing approvals over email, and manually matching invoices line by line before month…

Finance Automation Buyer's Guide for Australian Finance Teams: How to Choose, Scope & Measure Automation That Delivers (2026)

Most finance automation buying decisions are made the wrong way. Teams evaluate vendors on feature lists, watch polished demos, and sign contracts based on…