Finance Automation for Retail & eCommerce in Australia: How to Streamline AP, Inventory Reconciliation & Multi-Channel Reporting

Ordron28 min read

Australian retail and eCommerce finance teams are operating in one of the most data-intensive environments in any industry. You are simultaneously managing supplier invoices from dozens or hundreds of vendors, reconciling sales across Shopify, Amazon, eBay, your POS system, and your bank, handling GST across mixed-rate product lines, and trying to close the books in a timeframe that gives the business something useful. Most teams are doing a significant share of that work in spreadsheets.

The problem is not a lack of software. Most retail finance teams already have Xero or MYOB, a payment gateway, an inventory platform, and at least one marketplace integration. The gap is the connective logic between those tools. Data sits in silos. Reconciliation is done manually. Month-end close stretches to ten days or more because someone has to touch every transaction and match it by hand.

This article is for finance managers, CFOs, and operations leads in Australian retail and eCommerce businesses who want to understand which automation targets deliver the highest return, what a realistic implementation looks like, and how to build a business case that has actual numbers attached rather than aspirational projections lifted from a vendor slide deck.

Key Takeaways

- Retail and eCommerce finance teams face a unique combination of high transaction volumes, multi-channel data fragmentation, and GST complexity that makes manual processes especially costly.

- The five highest-ROI automation targets are accounts payable, bank reconciliation, inventory reconciliation, multi-channel revenue consolidation, and BAS/GST reporting.

- Automation does not require replacing your existing systems. The right approach builds connective logic across your current Xero or MYOB instance, your Shopify store, your marketplaces, and your inventory platform.

- A well-implemented 3-way match process for retail purchase orders eliminates the manual reconciliation bottleneck that causes most AP delays.

- Month-end close can realistically move from ten-plus days to three days with the right automation layer in place, without a single system replacement.

- The business case for retail finance automation is straightforward when you measure hours returned and error rates before and after go-live, not before.

Manual vs Automated: Retail Finance at a Glance

| Process | Manual Approach | Automated Approach | Realistic Time Saving |

|---|---|---|---|

| Accounts payable | Inbox monitoring, manual data entry, email approval chains | OCR capture, automated PO matching, exception-only routing | 60-80% reduction in AP cycle time |

| Bank reconciliation | Daily or weekly manual matching in Xero/MYOB | Auto-coded GL tags, rule-based matching, real-time dashboard | Up to 80% reduction in reconciliation time |

| Inventory reconciliation | Spreadsheet comparisons across warehouse and accounting records | Automated 3-way match across PO, GRN, and invoice | Near-elimination of end-of-period reconciliation backlog |

| Multi-channel revenue consolidation | Manual export from Shopify, marketplace, and POS, then manual journal entries | API-driven consolidation into accounting platform in real time | Month-end close reduced from 10+ days to 3 days |

| BAS/GST reporting | Manual classification of transactions by GST rate, spreadsheet summaries | Rule-based GST coding with exception flagging for mixed-rate items | 70%+ reduction in BAS preparation time |

Why Retail and eCommerce Finance Is Uniquely Complex in Australia

Retail finance complexity is not new. But the combination of factors that Australian retail and eCommerce businesses are dealing with in 2026 has made the manual approach genuinely unsustainable for any business operating at scale.

The Multi-Channel Data Problem

According to Australia Post's 2025 eCommerce Industry Report, more than 9.4 million Australian households shopped online in the previous year, and the majority of mid-sized eCommerce operators are selling across at least three channels simultaneously. That means your revenue data is split across Shopify or WooCommerce, Amazon AU, eBay, Catch (or its successor marketplaces), your own physical POS system if you operate bricks and mortar, and your payment gateway. Each of those platforms has its own settlement schedule, its own fee structure, its own currency handling for cross-border sales, and its own data export format.

When a finance team is pulling this together manually at month end, they are not just doing data entry. They are translating between incompatible formats, reconciling timing differences between when a sale happened and when the funds settled, and trying to net out platform fees before they can even start on revenue recognition. The ABS Retail Trade data for 2025-26 shows that Australian online retail turnover has continued to grow, which means the volume of these transactions is increasing. The manual approach does not scale.

GST Complexity Across Mixed Product Lines

Australian GST rules create a specific reconciliation challenge that finance teams in the UK or US do not face in the same way. The ATO's GST framework means that some product categories are GST-free (fresh food, most medical supplies, some educational materials) while others attract the standard 10% rate. For a retailer selling across categories, this means every transaction needs to be correctly classified before BAS can be prepared.

For eCommerce businesses selling to overseas customers, the rules shift again. Exports are generally GST-free, but low-value imported goods sold through online marketplaces have their own compliance obligations under the marketplace tax rules introduced by the ATO. If you are running this classification manually, errors compound across the period and BAS preparation becomes a week-long exercise in cleaning up misclassifications.

High Supplier Counts and Variable Payment Terms

A mid-sized Australian retailer might be managing 50 to 200 active suppliers, each with different payment terms, different invoice formats, and different approval requirements. Fast-moving consumer goods retailers dealing with FMCG suppliers often operate on 30-day payment terms with volume rebates that need to be netted against invoices. Fashion and apparel retailers might have seasonal suppliers on advance-payment terms alongside domestic suppliers on standard 30 or 60-day terms.

Managing this manually means your AP team is juggling spreadsheet trackers, email chains, and accounting platform entries simultaneously. The error rate is not a reflection of your team's capability. It is a structural consequence of high-volume manual processing.

The Month-End Close Problem

All of these factors converge at month end. A retail finance team running manual processes typically needs ten or more business days to close the books because every reconciliation task is sequential. You cannot start the revenue reconciliation until the settlement files are downloaded. You cannot close AP until the final batch of invoices is processed. You cannot finalise inventory until the warehouse count is reconciled against the accounting records. The result is financial data that is always lagging operational reality by two weeks or more.

The 5 Highest-ROI Automation Targets for Retail Finance Teams

Not all automation delivers equal return. Based on the work we have shipped across retail and eCommerce clients, these are the five areas where automation consistently returns the most hours and eliminates the most errors.

1. Accounts Payable Automation

AP is the single highest-volume manual process in most retail finance teams, and it is the one where the business case is easiest to demonstrate with numbers attached.

The problem in retail AP is not just the volume of invoices. It is the variability. Suppliers send invoices as PDFs, as EDI files, as emailed spreadsheets, and occasionally as paper documents. Invoice formats differ by supplier. Line items do not always match PO descriptions. Quantities can differ from what was received. A human reviewer catches these discrepancies eventually, but not before the invoice has passed through multiple hands and taken days to process.

Automated AP uses OCR (optical character recognition) combined with intelligent document understanding to read invoices regardless of format, extract the relevant fields, and match them against purchase orders and goods receipts in your system. Exceptions, meaning invoices where the match fails or a discrepancy is flagged, are routed to a human reviewer. Everything else processes automatically.

Across the AP automation work we have done, we are consistently achieving greater than 95% coding accuracy on invoices processed through intelligent document understanding, with around 75% of supplier invoices going through without any human intervention at all. For a retail business processing hundreds or thousands of invoices per month, that is a material shift in workload.

For a deeper look at what AP automation looks like in practice, see our accounts payable automation guide.

2. Bank Reconciliation

Bank reconciliation is often described as the unglamorous core of accounting, and it is. It is also one of the most time-consuming tasks for retail finance teams because of the sheer volume of transactions.

A retail business running Shopify and a POS system might have hundreds of daily transactions to reconcile, each needing to be matched to a bank line item. Settlement batches from payment gateways like Stripe, Afterpay, or Zip add another layer because the timing and the amounts do not map one-to-one to individual sales.

Automated bank reconciliation uses rule-based matching logic to auto-code transactions by GL account based on the payee, the transaction description, and the amount range. Rules can be built for settlement batches, recurring supplier payments, payroll, and platform fees. The result is that the reconciliation is largely complete before anyone in the finance team sits down to review it. You are reviewing exceptions, not doing the reconciliation.

We implemented exactly this approach for a freight operator running AR on Xero. The result was an 80% reduction in reconciliation time, with real-time aged-receivables visibility replacing the lagged reporting that had been the norm. The same logic applies directly to retail and eCommerce environments. You can read more about the reconciliation automation approach in our reconciliations automation guide.

3. Inventory Reconciliation

Inventory reconciliation is where retail finance teams spend a disproportionate amount of time because the data comes from systems that do not naturally talk to each other. Your warehouse management system or 3PL records stock movements. Your eCommerce platform records sales. Your accounting platform records cost of goods sold. Keeping these three in sync manually is a monthly exercise in finding and explaining variances.

Automated inventory reconciliation builds the connective logic between these systems so that stock movements, sales, and COGS entries stay in sync continuously rather than being reconciled at period end. The automation layer reads GRN data from your warehouse, matches it against POs in your accounting platform, and posts the corresponding COGS entries as stock is sold. Variances are flagged in real time rather than discovered at month end.

For retail businesses using FIFO or weighted average cost methods for inventory valuation, the automation layer also handles the cost calculation, applying the correct valuation method to each stock movement without manual intervention.

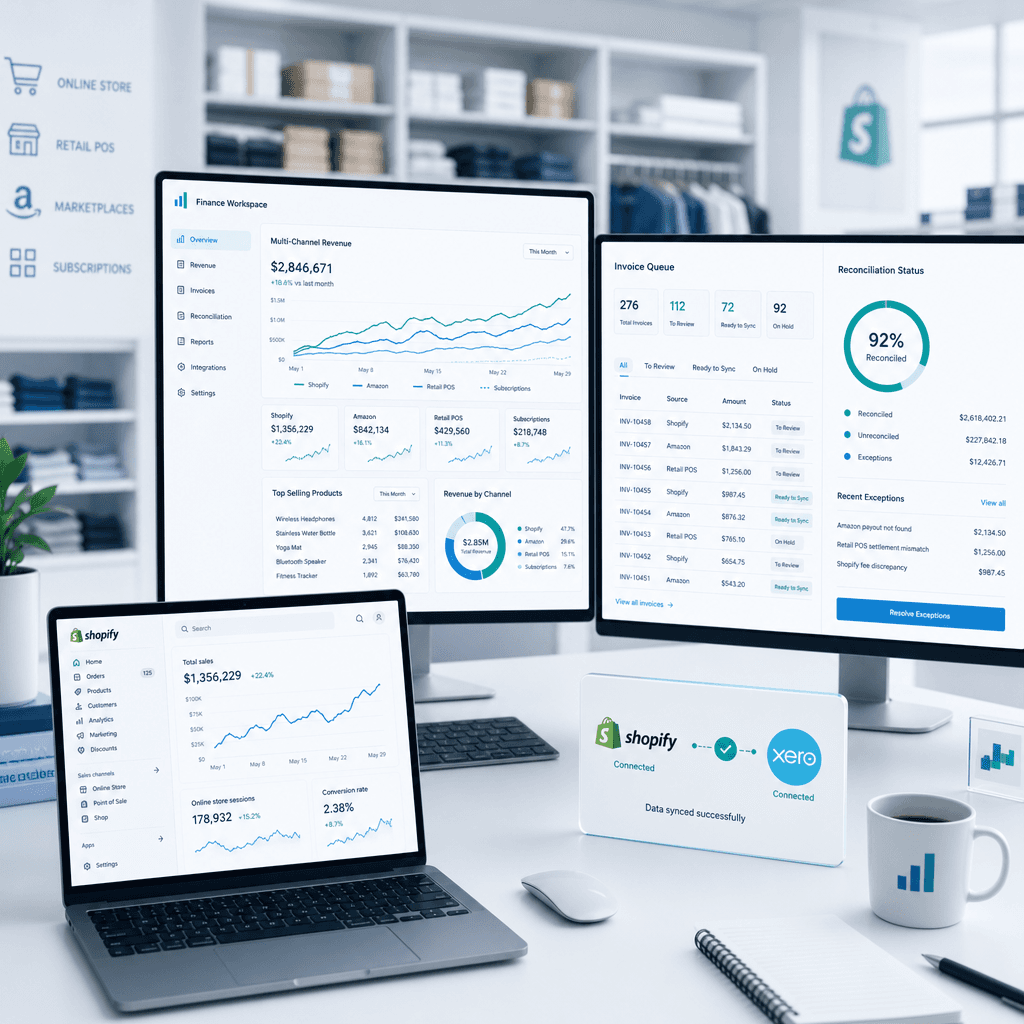

4. Multi-Channel Revenue Consolidation

This is the automation target that has the most direct impact on month-end close time. If you are selling across Shopify, Amazon, eBay, and a physical POS, consolidating your revenue for the period means downloading settlement reports from each platform, converting them to a common format, netting out platform fees, handling currency conversion for any international sales, and posting journal entries that match your chart of accounts.

Done manually, this takes days. Done with an automation layer that has direct API connections to each platform and rule-based logic for fee handling and journal posting, it happens continuously and the data is current at any point in the month.

The Shopify-to-Xero integration is the most common starting point for Australian eCommerce retailers. There are native integrations available, but they often require customisation to handle the specific settlement timing, fee netting, and GST treatment that a given retailer needs. Our Xero automation platform page covers the specifics of what that integration layer looks like.

For retailers on MYOB, the same principles apply through a different integration pathway. See our MYOB automation platform page for detail on the MYOB-specific implementation.

5. BAS and GST Reporting

BAS preparation is the compliance task that retail finance teams dread most. The combination of mixed GST rates across product categories, export sales, marketplace sales with their own GST obligations, and the sheer volume of transactions that need to be correctly classified makes manual BAS preparation both slow and error-prone.

Automated GST reporting builds classification rules into the transaction processing layer so that every sale, every purchase, and every fee is correctly coded at the point of entry rather than being reviewed and corrected at BAS time. Exceptions, such as transactions that do not match any existing rule, are flagged for human review. The remainder go through coded correctly.

For eCommerce businesses selling through marketplaces that are themselves registered for GST under the marketplace rules, the automation layer also handles the distinction between marketplace-remitted GST and retailer-remitted GST, which is a common source of BAS errors in manual processes.

Building Your Platform Stack: Xero or MYOB + Shopify + Marketplace Integrations + Automation Layer

One of the most persistent myths in retail finance automation is that you need to replace your existing systems before you can automate meaningfully. This is not true, and in most cases it is not even good advice.

Replacing a core accounting platform mid-growth is expensive, disruptive, and time-consuming. The migration risk alone is significant. More importantly, it is usually unnecessary. The right automation approach treats your existing stack as the constraint to route around, not the problem to solve.

The standard retail finance stack for an Australian eCommerce business looks something like this:

- Accounting platform: Xero or MYOB (occasionally NetSuite or Cin7 for more complex operations)

- eCommerce platform: Shopify (dominant for Australian DTC retailers), WooCommerce, or BigCommerce

- Marketplaces: Amazon AU, eBay, Catch, or similar

- POS: Square, Lightspeed, or a legacy system

- Inventory management: Cin7, DEAR, Unleashed, or a warehouse management system

- Payment gateways: Stripe, Afterpay, Zip, PayPal

The automation layer sits across all of these, pulling data from each source, applying transformation and matching logic, and writing clean records into your accounting platform. It does not replace any of them.

This is where the connective logic does the actual work. A Shopify store with a native Xero integration might push daily settlement summaries into Xero automatically, but it will not handle fee netting, GST classification for mixed-rate products, or multi-currency conversion without additional logic built into the integration layer. That additional logic is where most of the manual work currently lives, and it is exactly what automation addresses.

For an independent comparison of the available automation tools in the Australian market, our finance automation tools comparison is worth reading before committing to a platform.

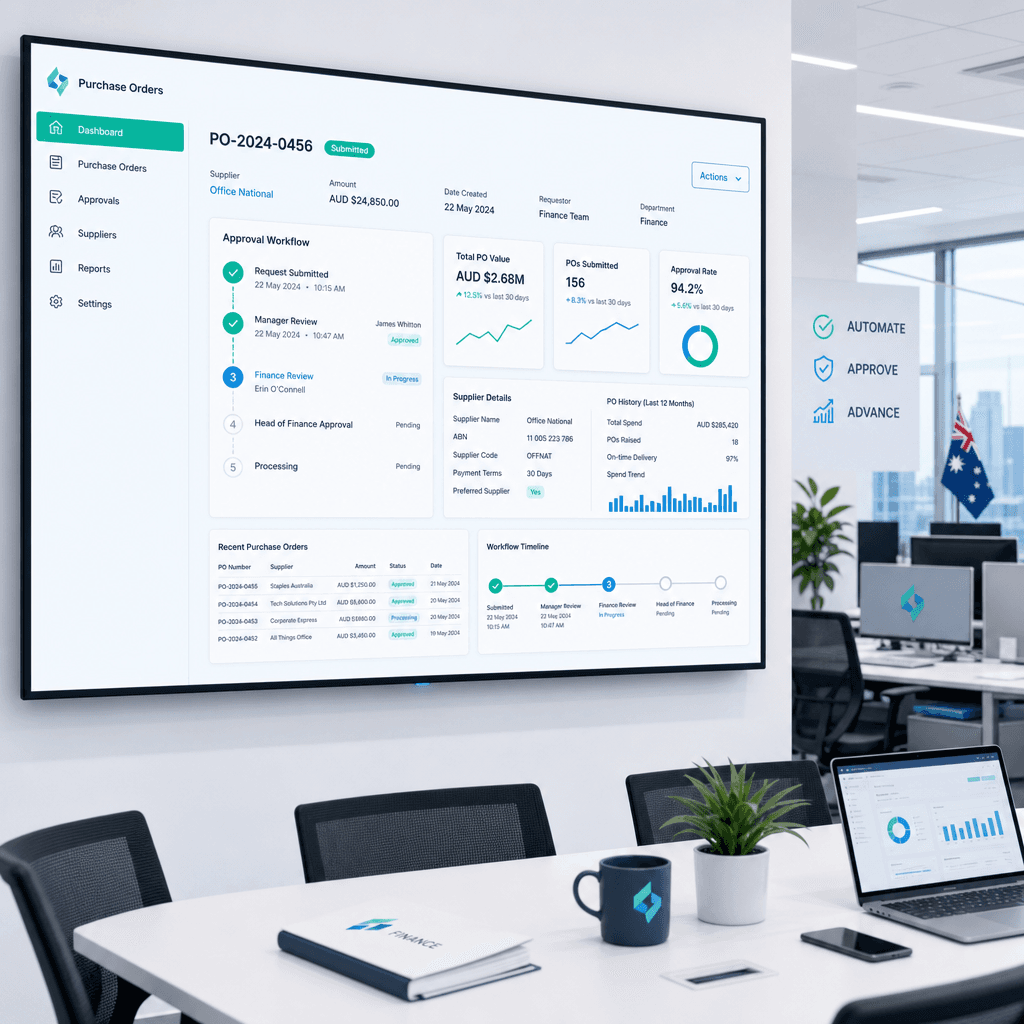

Real Workflow Example: Automated 3-Way Match for Retail Purchase Orders

The 3-way match is the gold standard for AP accuracy in retail: you match the supplier invoice against the purchase order and against the goods receipt note (GRN) before approving payment. Done manually, it is reliable but slow. Done with automation, it is reliable and fast.

Here is what the automated workflow looks like in practice for a retail business:

Step 1: Invoice capture. A supplier emails an invoice to a designated AP inbox. The automation layer picks up the email, extracts the invoice attachment, and runs it through OCR and intelligent document understanding. The system reads the supplier name, invoice number, invoice date, line items, quantities, unit prices, and totals, regardless of the invoice layout.

Step 2: PO matching. The extracted line items are matched against open purchase orders in the accounting platform. If the invoice number, supplier, and line item quantities and prices match the PO within tolerance, the match is confirmed automatically.

Step 3: GRN matching. The confirmed PO match is then checked against the goods receipt note from the warehouse or 3PL system. If the quantities received match the quantities invoiced within the accepted tolerance, the 3-way match is complete.

Step 4: Automated posting. Matched invoices are posted to the accounting platform with the correct GL coding, cost centre allocation, and GST treatment applied automatically. The invoice is scheduled for payment on the due date based on the supplier's payment terms.

Step 5: Exception routing. Invoices where the match fails, or where the variance exceeds the accepted tolerance, are routed to the relevant human reviewer with the discrepancy clearly flagged. The reviewer sees only the exceptions, not the full invoice queue.

This workflow is not theoretical. It is the structure we have built for retail and distribution clients, and the outcomes are consistent: greater than 95% coding accuracy, 75% of invoices processing without human intervention, and AP cycle time measured in minutes per batch rather than hours.

I saw a version of this validated in a different industry context when we built automation for a national logistics provider whose SharePoint-based AP process was taking four hours per invoice batch. By plugging OCR and workflow logic into the existing SharePoint environment without introducing any new software, we cut that cycle time from four hours to fifteen minutes per batch. The principle is identical for retail AP: the connective logic is the lever, not the system.

Building the Business Case for Retail CFOs

The business case for retail finance automation fails when it is built on aspirational projections. It succeeds when it is built on measured baselines and realistic outcome ranges drawn from comparable implementations.

Here is the framework that works.

Step 1: Measure Your Current State

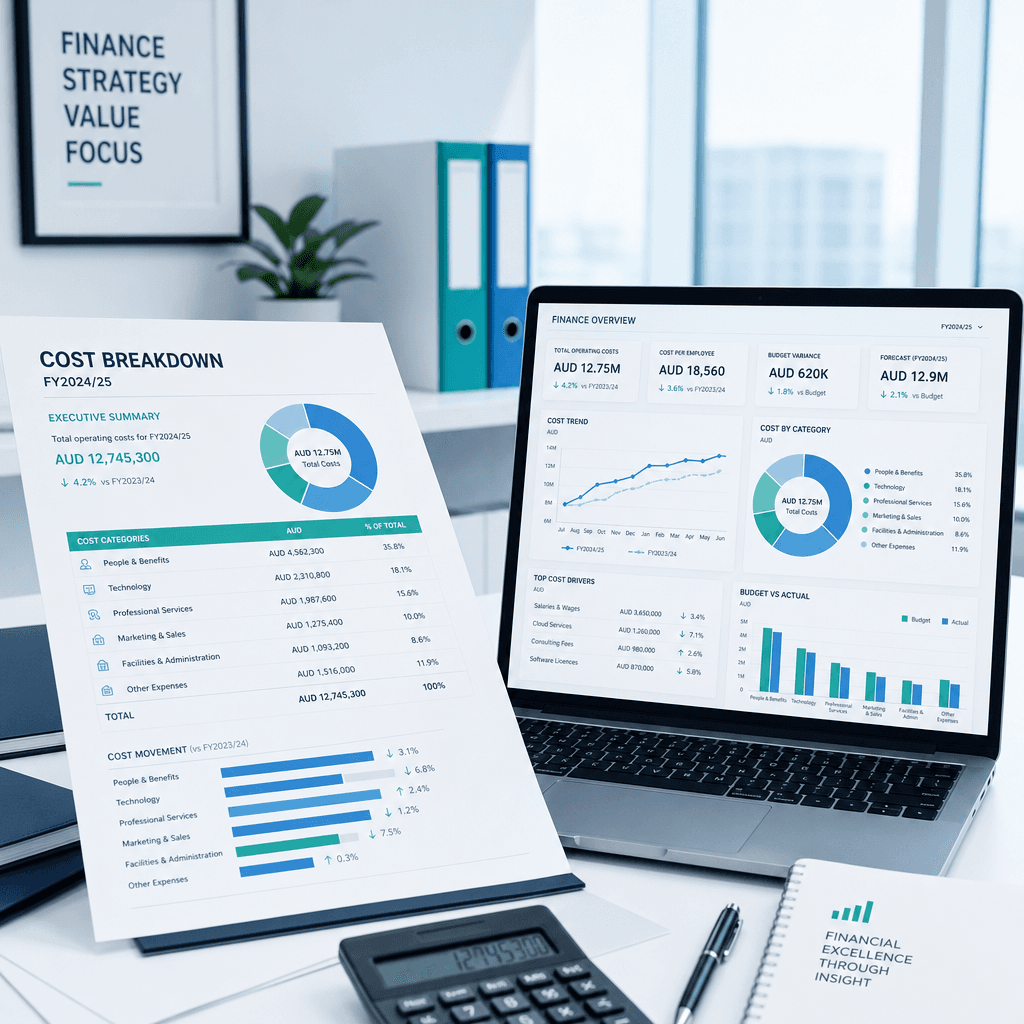

Before you can build a case, you need to know what you are currently spending. That means counting the actual hours your finance team spends each month on AP processing, reconciliation, revenue consolidation, and BAS preparation. Most finance managers can estimate this within a reasonable range. If you cannot, a two-week time-tracking exercise across the team will give you the data.

Add to this the cost of errors: late payment penalties from missed supplier terms, BAS corrections and ATO interest charges, inventory write-offs that could have been caught earlier with better reconciliation, and any cost of over-hiring to keep up with volume growth.

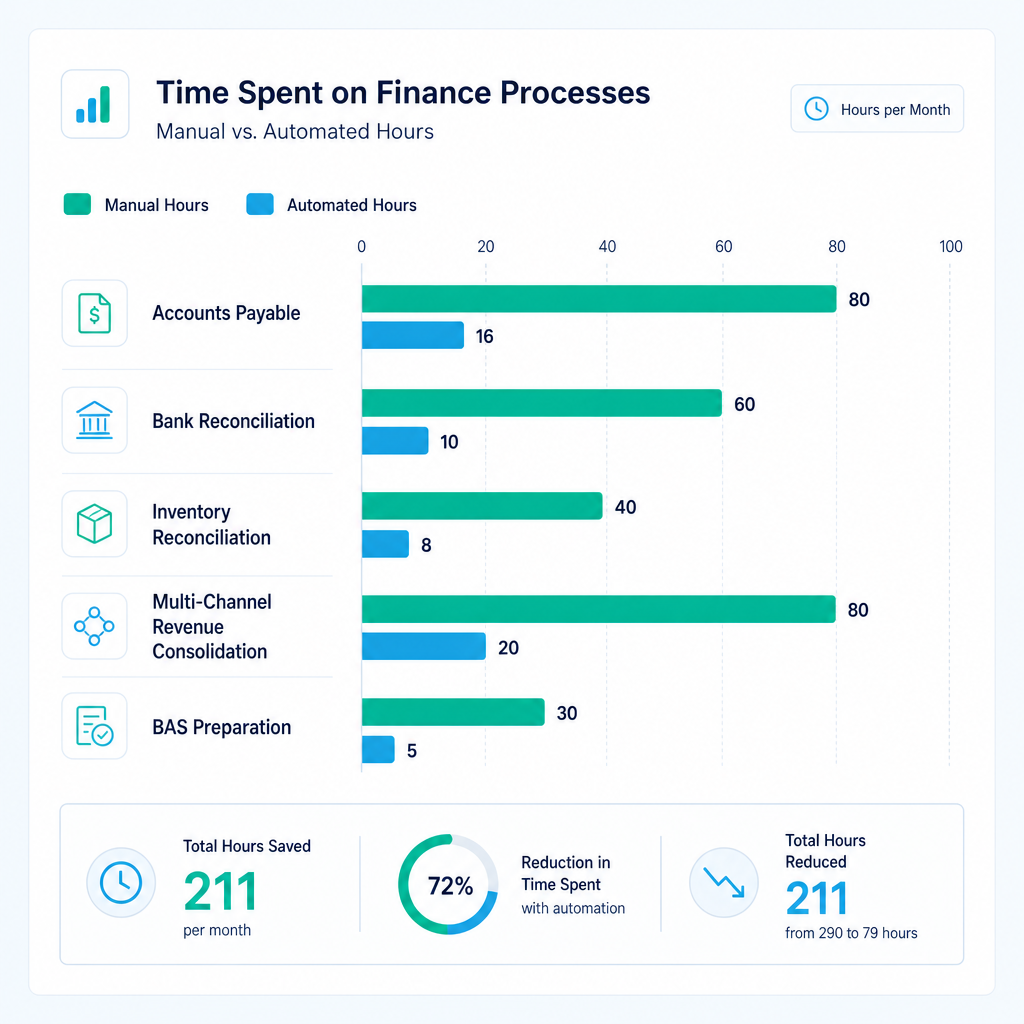

Step 2: Apply Realistic Reduction Ranges

Based on the work we have shipped across retail, logistics, distribution, and manufacturing clients, these are realistic reduction ranges for each process area:

- AP processing time: 60-80% reduction

- Bank and AR reconciliation time: 75-80% reduction

- Multi-channel revenue consolidation: 80%+ reduction

- BAS preparation time: 70%+ reduction

- Month-end close duration: from 10+ days to 3 days in well-scoped implementations

These are not vendor projections. They are anonymised outcomes across industries from engagements where we measured the result after go-live.

Step 3: Calculate the Return on Hours Returned

Convert the hours saved to a dollar figure using your fully loaded staff cost. If your finance team earns an average of $75,000 per year (roughly $38 per hour at standard working hours), and automation returns 40 hours per month across the team, that is $1,520 per month in direct labour cost reduction, or $18,240 per year. For a larger team with higher volumes, the numbers scale significantly.

Add the error reduction value. A single BAS correction with ATO penalties and interest can cost thousands of dollars. Eliminating that risk has a value even if it is harder to quantify precisely.

Step 4: Compare Against Implementation Cost

Retail finance automation implementation costs in Australia typically range from $15,000 to $60,000 depending on the complexity of the integrations required, the number of channels and systems involved, and the degree of customisation needed. Ongoing maintenance and support adds to the annual cost.

A business returning $18,240 per year in direct labour savings alone, on a $25,000 implementation, achieves payback in under 18 months. A business returning 160 hours per month, as we achieved for a logistics operator in a comparable project, sees payback in a matter of months.

For a structured approach to building this case, our finance automation ROI guide walks through the methodology in detail. And if you want a rapid assessment of where your current finance stack sits, our finance health check is the right starting point.

You can also review anonymised case studies from our completed engagements to see what measured outcomes look like across different business types and sizes.

Common Mistakes When Automating Retail Finance

Retail finance automation projects fail for predictable reasons. These are the ones we see most often.

Mistake 1: Starting With a Platform Decision Instead of a Problem Definition

The most common mistake is beginning the automation conversation with "which platform should we use" rather than "which process is costing us the most and why". Platform selection without a defined problem leads to over-engineered solutions, lengthy implementation timelines, and outcomes that cannot be measured because no baseline was established.

The right starting point is always the process. What is the highest-volume manual task in your finance team right now? Where do errors occur most frequently? Which process is blocking month-end close? Answer those questions first, then select the tools that address them.

Mistake 2: Assuming You Need to Replace Your Accounting Platform

This is the most expensive mistake, and it is usually made based on advice from a software vendor with an interest in a platform sale. Xero and MYOB are both capable platforms for retail finance automation when the right integration and automation layer is built across them. Replacing either one mid-growth introduces migration risk, staff retraining cost, and months of disruption for a marginal improvement in outcomes.

We build automation across legacy systems without replacing them. That is not a marketing position. It is the practical result of working with businesses that cannot afford the disruption of a full system replacement and do not need one to get the automation benefit they are looking for.

Mistake 3: Automating a Broken Process

Automation amplifies whatever process it is applied to. If your current AP process has structural flaws, such as unclear approval hierarchies, duplicate supplier records, or inconsistent GL coding conventions, automating it will make those flaws faster and more expensive. Before you automate, clean up the process. Standardise your supplier master data. Document your approval thresholds. Agree on your chart of accounts structure. This groundwork takes days, not weeks, and it makes the automation significantly more effective.

Mistake 4: Underestimating the Integration Complexity of Marketplaces

Shopify has a well-documented API and good native integration options for Xero and MYOB. Amazon and eBay are more complex. Settlement reports from marketplace platforms include fees, refunds, advertising credits, FBA fulfilment costs, and currency adjustments all in a single file, and the format changes periodically. Building a reliable automation layer across Amazon requires explicit handling of each of these line item types, and it requires ongoing maintenance when Amazon changes its report format.

Retailers who underestimate this complexity end up with an automation layer that handles Shopify well and still requires manual processing for their marketplace channels. That is better than nothing, but it is not the full solution.

Mistake 5: Not Measuring the Before State

This is the mistake that makes it impossible to demonstrate ROI. If you do not measure how long your current AP process takes, how many hours per month reconciliation consumes, or what your current BAS error rate is, you have no baseline against which to measure the outcome after go-live. The automation may have worked exactly as intended and you will not be able to prove it.

Measure the before state before you start. It takes a few hours and it is the single most important input into a credible business case.

Mistake 6: Ignoring the Exception Management Design

Every automation system produces exceptions: transactions that do not match any rule, invoices with discrepancies, GST classifications that need human review. The quality of your exception management design determines whether automation reduces workload or simply moves the bottleneck.

A good exception management design means that every exception is routed to the right person with the right context already surfaced. The reviewer sees the transaction, the rule it failed, and the recommended action. They approve or correct and move on. A poor exception management design means that exceptions pile up in an inbox with no context and no prioritisation, and the finance team spends more time managing exceptions than they saved on the automated transactions.

Design the exception flow with as much care as you design the automation rules.

References

-

Australia Post eCommerce Industry Report 2025, Australia Post's annual report on the state of eCommerce in Australia, covering household penetration, category growth, and channel trends. Used to support claims about multi-channel selling prevalence among Australian online retailers.

-

ABS Retail Trade Data 2025-26 (Australian Bureau of Statistics), The ABS monthly retail trade series covering turnover by industry and channel. Used to support claims about the growth trajectory of Australian online retail and the increasing transaction volume facing retail finance teams.

-

ATO GST Guidance for Online Sales (Australian Taxation Office), The ATO's published guidance on GST obligations for online retailers, including marketplace rules for low-value imported goods and the treatment of exports. Used to support the BAS and GST reporting section.

-

Xero Platform Documentation and App Marketplace (Xero Australia), Xero's official documentation covering API capabilities, third-party integrations, and the Shopify and marketplace connectors available in the Australian market.

-

MYOB AccountRight Documentation (MYOB Australia), MYOB's official documentation covering AccountRight's inventory accounting features, API capabilities, and integration ecosystem relevant to Australian retail finance teams.

-

ACCC Digital Platform Services Inquiry (Australian Competition and Consumer Commission), ACCC reporting on the dominance of digital platforms in Australian eCommerce and the competitive dynamics affecting marketplace fee structures and retailer obligations.

Frequently asked questions

- Can I integrate Shopify directly with Xero for automated reconciliation?

- Yes, and most Australian Shopify retailers running Xero should have this integration in place as a minimum. Shopify has a native Xero integration through its app store, and there are third-party connectors including A2X that provide more granular control over how settlement batches are split and posted. The native integration handles the basics, but most retailers selling across multiple channels or with complex GST requirements will need a configured integration layer on top to handle fee netting, GST classification, and timing differences correctly.

- How does GST work for marketplace sales on Amazon AU and eBay?

- Under the ATO's marketplace rules, platforms like Amazon AU and eBay are required to collect and remit GST on sales of goods valued up to $1,000 AUD made through their platforms by overseas sellers. For Australian-registered sellers, you generally remain responsible for reporting and remitting GST on your sales through these platforms. GST coding for marketplace sales needs to distinguish between transactions where GST has been remitted by the platform and transactions where you are responsible for remittance. Getting this wrong is a common source of BAS errors for eCommerce retailers.

- Can automation handle inventory valuation methods like FIFO or weighted average cost?

- Yes. Inventory valuation automation works by building the valuation logic into the integration layer between your inventory management system and your accounting platform. The automation layer reads stock movements and applies the relevant cost method, whether FIFO, weighted average, or specific identification, to calculate the COGS entry for each movement. This is standard functionality in platforms like Cin7, DEAR, and Unleashed when connected to Xero or MYOB, and it can be extended with custom automation logic for more complex scenarios.

- How long does a retail finance automation implementation take?

- For a mid-sized Australian retailer, a focused automation engagement covering AP, bank reconciliation, and Shopify-to-Xero integration typically takes four to eight weeks from scoping to go-live. Multi-channel implementations covering additional marketplace integrations and automated inventory reconciliation run eight to twelve weeks. The timeline is driven by the complexity of the integrations required and the quality of the baseline data in your current systems.

- What does retail finance automation typically cost in Australia?

- Implementation costs for Australian retail finance automation engagements range from approximately $15,000 to $60,000 AUD including GST, depending on scope. A focused AP automation engagement sits at the lower end of that range. A multi-channel eCommerce implementation covering Shopify, marketplace integrations, inventory reconciliation, and BAS reporting sits at the higher end. Ongoing maintenance typically adds $1,000 to $3,000 per month. Most implementations achieve payback within twelve to twenty-four months based on direct labour cost savings alone.

- Should I use Xero or MYOB for retail finance automation in Australia?

- Both platforms are viable for retail finance automation in Australia. Xero has a larger ecosystem of third-party integrations and is the dominant platform among Australian eCommerce retailers. MYOB AccountRight is often a better fit for retailers with more complex inventory accounting requirements, multi-entity structures, or existing MYOB investments. For most direct-to-consumer eCommerce businesses, Xero is the path of least resistance for automation. The automation approach is similar for both platforms.

- Can retail finance automation handle multi-entity consolidation?

- Yes, though this adds a layer of complexity. Multi-entity consolidation for retail businesses requires inter-entity transaction elimination in addition to standard automation logic. The automation layer can handle this by tagging inter-entity transactions at the point of entry and running automated elimination entries as part of the consolidation process. The result is a consolidated view of the group's financials that updates continuously rather than being assembled manually at period end.

- When is the right time to start automating retail finance?

- The honest answer is: before you feel ready. Most retail finance teams wait until the pain is severe enough that automation feels urgent, and by that point they have already absorbed months or years of unnecessary manual work and errors. The right time to start is when you can clearly identify a process that is consuming a disproportionate amount of your team's time and producing a measurable error rate. If you are unsure where to start, complete a finance health check to identify your automation quick wins, implement them, measure the result, and build from there.

Ordron

Finance automation team, Sydney

Ordron builds the finance automation infrastructure that runs AP, AR, reconciliations and reporting on autopilot for Australian mid-market businesses.

More from the Ordron Insights catalogue

Selected by topic. Updated as the agent publishes.

How to Automate Purchase Orders in Australia: A Practical Guide for Finance Teams

Most Australian finance teams are still processing purchase orders the same way they were a decade ago: an email chain, a spreadsheet, a PDF attachment, and…

Finance Automation ROI Benchmarks for Australian Businesses: What Good Actually Looks Like

Every vendor selling finance automation will show you a projected ROI slide. The numbers are always impressive: cost savings in the hundreds of thousands,…

How Much Does Finance Automation Cost in Australia? A Pricing Guide for CFOs (2026)

Ask three finance automation vendors for a quote and you will get three completely different answers. One will talk about platform licensing, another will lead…